Activity-based costing (ABC) - What is the activity-based costing method?

Activity-based costing (ABC) is a method of assigning operational costs within a company to the products or services the company sells.

Pricing your products is an important aspect of your business. Read more on our blog about how to boost your profits using pricing strategies.

The ABC method takes overhead and indirect costs, and links them to related goods and services.

The ABC method is most commonly used in the manufacturing sector as it is easier and more logical to find the total cost of all activities required to make a product.

Many companies use the cost of goods sold (COGS) as a factor to price their products. However, this method of determining how much it costs to make a product does not directly allocate overhead to the products.

How does activity-based costing work?

In this section, I have provided step-by-step instructions on how to use activity-based costing, along with an in-depth example.

Identify activities and cost pools

To use the ABC method, you will first have to understand how to assign costs to activities.

For example, let’s say your company makes 2 products, backpacks, and purses. Let’s say the overhead/indirect costs you are trying to allocate amounts to £1 million. These are overhead or indirect costs, such as equipment depreciation, manufacturing, or employee salaries.

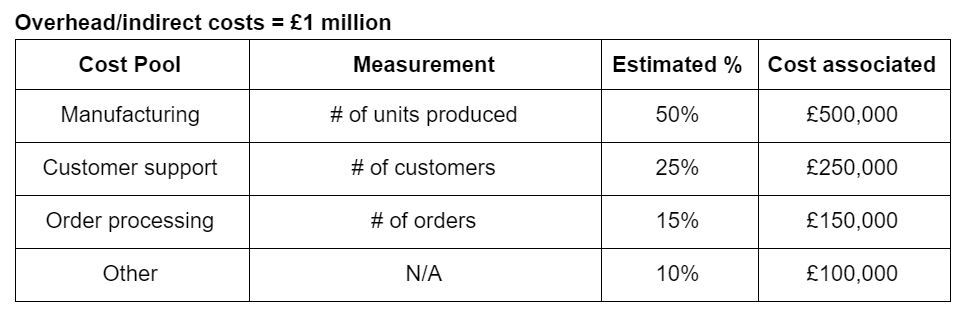

First, you will need to identify the activities you are trying to allocate. You will then look at the £1 million, and create “cost pools” (or categories) explaining how that money was spent. While you create different cost pools, you will also need to determine how you will measure them.

For instance:

- One cost pool could be order processing, which will be measured by the number of orders.

- Another cost pool could be customer service, which will be measured by the number of customers you have.

- Another cost pool could be manufacturing, which will be measured by the number of units produced.

It is also recommended to have a cost pool for ‘other’, which are costs that cannot be allocated to other cost pools. This could include something like a lease on the factory or office, which does not fit in with the other categories and cannot be assigned to a specific product.

Allocate overhead to the cost pools

Once you have created a list of your cost pools and how you will measure them, you will need to spread the £1 million between them. This is an estimate of how much of the £1 million is used for each cost pool. To identify this estimate, you will need to interview employees to get an idea of how much time (and money) is spent on each activity.

It is up to you how you want to conduct these interviews, but the main purpose of this is to identify how the money is spread throughout the activities. For instance, if you have an employee who works in customer service as well as order processing, you can ask them how much time he/she spends on each activity.

From there, you can estimate that 50% of the £1 million is used for manufacturing, 15% is used for order processing, 25% is used for customer support, and 10% is used for other. From the estimated percentages, you can find the cost associated with each cost pool as seen below.

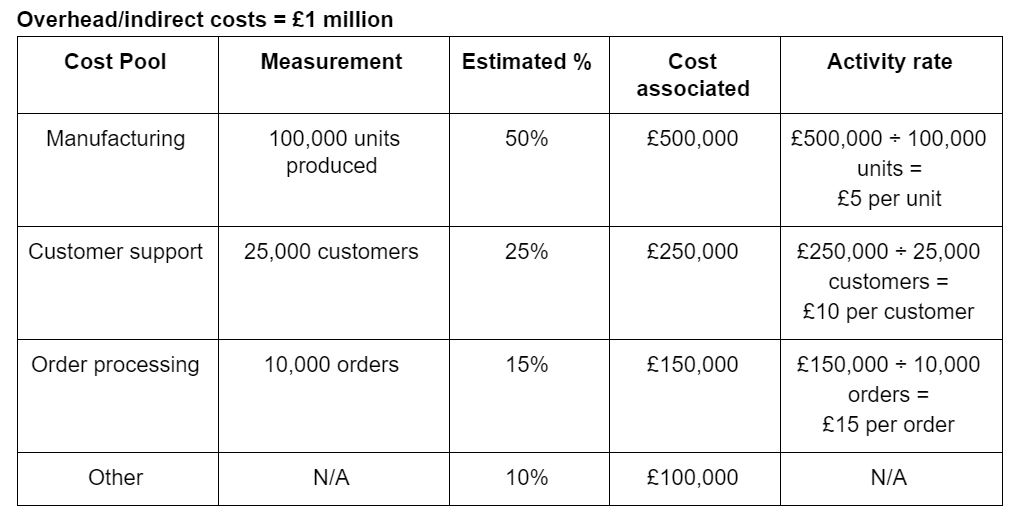

Calculate the activity (cost pool) rate

Once you have the estimated percentages and costs associated with each cost pool, you will need to calculate the activity rate. The activity rate is calculated by the cost divided by the measurement, as seen in the chart below.

At this stage, you need to know the estimated measurements for the time frame you are calculating. For instance, you estimate that this year you will manufacture 100,000 units of backpacks and purses. You then divide the cost associated (in this case £500,000) by the 100,000 units produced to get an activity rate of £5 per unit.

Use the activity rates to assign overhead to cost products

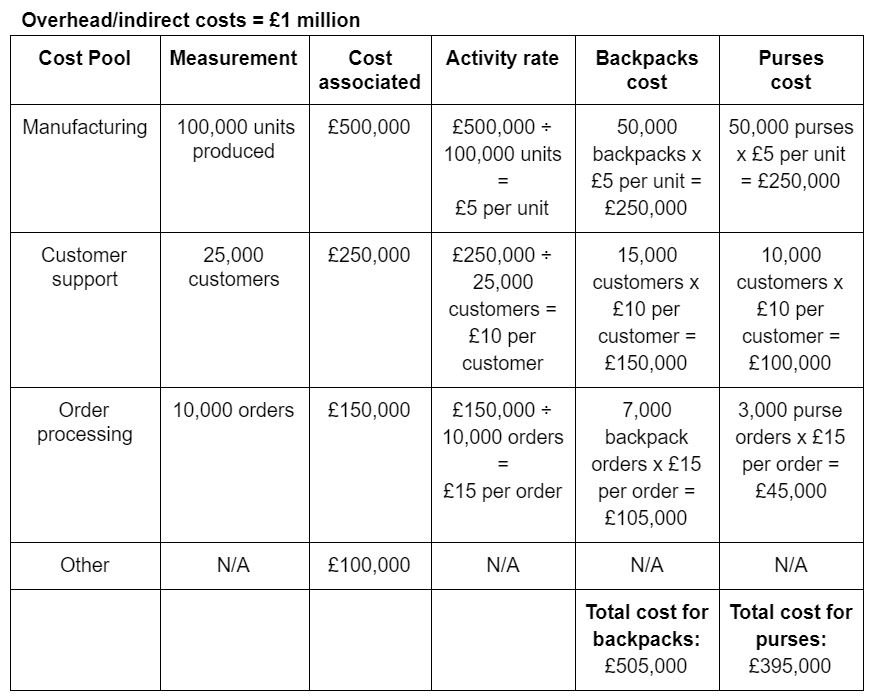

Now that you have calculated the activity rate for each cost pool, you can divide it up between the products you sell. In this example, we have a company that sells backpacks and purses.

Assigning overhead example:

To make it simple, we’ll say that an equal amount of backpacks and purses were produced for this time period. Therefore, 50,000 backpacks and 50,000 purses were produced, with a manufacturing cost of £5 per unit. From this data, you can calculate that it costs £250,000 to produce the backpacks, and £250,000 to produce the purses.

To make it more interesting, we’ll say that there were more backpack orders than purse orders. Out of the 10,000 total orders, 7,000 were for backpacks, and 3,000 were for purses. With an order processing cost (activity rate) of £15 per order, it costs £105,000 for order processing for backpacks, and £45,000 for purses.

Since there are more backpack orders than purse orders, the customer support agents will spend more time on customers who ordered backpacks, than purses. Let’s say out of 25,000 customers, 15,000 are for backpacks, and 10,000 are for purses.

Once you have calculated the cost of each activity (cost pool) per product, you can add up the total indirect costs associated with each product.

From this data, you can determine that you are producing the same amount of backpacks and purses, however, there are more orders and customers for backpacks. Therefore, more overhead costs are going into producing backpacks, than purses.

You may also notice that the total cost for backpacks (£505,000), and purses (£395,000) do not add up to our original £1 million in overhead costs. The reason for this is that we did not allocate any money from the ‘Other’ cost pool to the products, as they are not activities related to the products.

That is the end of the ABC process. ABC helps get a better idea of what the specific indirect costs are for the backpack division and purse division instead of applying one factory/office-wide overhead.

Activity-based costing vs. traditional costing

The main difference between the two costing methods is how the overhead rates are calculated.

With traditional costing, there is only one company/plant-wide overhead rate. It is simpler to calculate but does not provide a precise way to assign activities to different products. An example of how the overhead rate would be calculated with traditional costing is overhead divided by labour hours.

With activity-based costing, there are multiple overhead (or activity) rates. This will allow you to accurately match activities (from cost pools) to products, providing more precise costing.

Traditional costing is much easier to implement, whereas the ABC method requires a lot of extra work. In order to implement the ABC method, you will need to do things like interview employees to decide which items will go in which cost pool, figure out which cost pools you should and shouldn’t have, and make estimates and trials to decide what is best for your business.