Credit derivative - What is a credit derivative?

A credit derivative is an instrument that allows you to separate the credit risk from an asset, to then be traded to a different party.

Looking to launch a new business and need some financial backing? Check out our guide on how to get financial backing from a bank or investor.

In a creditor/debtor relationship, a credit derivative allows the creditor to shift the risk of the debtor’s non-payment to a third party.

Credit derivatives can be used for any financial assets such as bank loans, corporate debt, and trade receivables. Credit derivatives are the bilateral contracts between the two parties, and the buyer usually pays a fee to the party that is taking over the risk.

Credit derivative example

As an example, let’s say that a business wants to borrow £50,000 from a bank over a 5 year period. This business has a poor credit history, and so the bank will only issue the loan if they agree to purchase a credit derivative. This credit derivative allows the bank to transfer the risk of non-payment to a third party.

The fee that they pay for the credit derivative is usually an annual fee paid over the lifetime of the loan. If the company defaults, the third party will be responsible for any remaining balance or interest. If the company does not default, the third party gets to keep the credit derivative fee.

Ultimately, if everything goes well, the bank is covered for the risk of default by the third party, the company receives the loan, and the third party is paid the credit derivative fee.

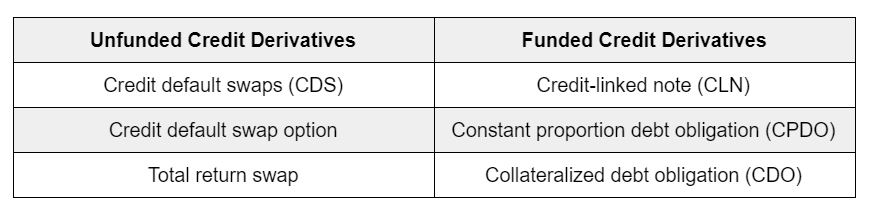

Categories of credit derivatives

There are two categories of credit derivatives, unfunded, and funded.

An unfunded credit derivative is a contract between two parties in which each party is responsible for making payments under the contract. The most common type of unfunded credit derivative is credit default swaps (CDS).

A funded credit derivative is where the party which takes responsibility for the risk makes an initial payment to cover any future defaults or credit events. The most common type of funded credit derivative is the credit-linked note (CLN).

Types of credit derivatives

There are several different types of credit derivatives falling under the two categories. I’ll explain the main ones below.

Credit default swaps (CDS)

This is the most common type of credit derivative. In a credit default swap, the seller (person who takes on the risk) negotiates a fee (either upfront or continuous), in order to compensate the buyer if they were to default, or were unable to pay.

There are a few different types of credit default swaps, depending on the number of entities involved. The main two are credit default swaps on single entities, and credit default swaps on baskets of entities.

Credit-linked note (CLN)

This is the most common type of funded credit derivative and is also known as a credit default note. In a credit-linked note, the risk of default is transferred to the investors who take on the risk in exchange for a higher return.

Investors purchase CLNs from a trust that pays a principal/coupon payment throughout the time of the loan. Although they take on the risk of default, if that does not occur, they earn a higher return than other bonds.

Credit default swap option

A credit default swap option, also known as a credit default swaption, can be added as an option to a credit default swap (CDS). It is an optional add-on to a CDS to purchase buyer or seller protection for an entity for a specific future period in time.

Constant proportion debt obligation (CPDO)

Constant proportion debt obligations are very complex financial instruments that essentially allow investors a high rate of return with lower default risk. They are created through a special purpose vehicle (SPV) which issue credit default swaps against bonds. These swaps transfer gains from the bond to the investor, who then buys and sells the derivatives on an underlying index.

Total return swap

A total return swap is a process of transferring all risk (both market and credit) of an asset. In this credit derivative, the assets are usually bonds and loans. The payer of this derivative can remove all economic risk without selling it. The receiver has access to the asset without owning it, in exchange for the default risk.

Collateralized debt obligation (CDO)

Collateralized debt obligation (CDO) is a credit derivative where the asset is sold to multiple investors who each take on part of the risk. For instance, a bank can sell a loan divided to multiple investors, who then each take on the risk that comes along with the loan.

This way, the bank no longer has the risk and has money to make other loans, while the investors take on the risk, but also gain profit through interest.