Provision - What is a provision?

A provision is an amount set aside from a company’s profits to cover an expected liability or a decrease in the value of an asset, even though the specific amount might be unknown.

Stay on top of your company finances with Debitoor invoicing software, designed for sole traders, freelancers, and small businesses. Try Debitoor free for 7 days.

A provision is not a form of savings; instead, it is a recognition of an upcoming liability.

The IFRS sometimes calls a provision a reserve; however, reserves and provisions are not interchangable concepts. Whereas a provision is intended to cover upcoming liabilities, a reserve is part a business's profit, set aside to improve the company's financial position through growth or expansion.

Provisions in accounting

In accounting, the matching principle states that expenses should be reported in the same financial year as the correlating revenues. This is because costs that belong to a certain year can become misleading if accounted for in previous or future financial years.

Provisions therefore adjust the current year balance to be more accurate by ensuring that costs are recognised in the same accounting period as the relevant expenses.

Provisions are recognised on the balance sheet and are also expensed on the income statement.

Types of provision in accounting

The most common type of provision is a provision for bad debt. A provision for bad debt is one that has been calculated to cover the debts encountered during an accounting period that are not expected to be paid.

This provision is usually included in the budget created by a company and can be estimated based on past experience with bad debt amounts as well as industry averages.

Other common kinds of provisions in accounting include:

- Restructuring Liabilities

- Provisions for bad debts

- Guarantees

- Depreciation

- Accruals

- Pension

How to create a provision

There are a number of factors that could cause a company to create provisions; however, there are certain requirements that must be fulfilled before a financial obligation can be viewed as a provision. These include:

- The company must perform a reliable amount of regulatory measurement of the obligation. The measurement must be undertaken by company management.

- It must be probable that the obligation results in a financial drag on economic resources.

- An obligation must be a result of events that will advance the balance sheet date and could result in a legal or constructive obligation.

- An obligation must be determined to be probable, but not certain. It must be estimated to have a more than 50% probability of occurring.

Tax and provisions

The way a provision is handled for tax purposes depends on whether it is a general provision or a specific provision.

A general provision is not allowed as a tax deduction. A specific provision - in which specific debts are identified - is allowed as a tax deduction if there is documentary evidence to indicate that these debts are unlikely to be paid.

Provisions and Debitoor

With Debitoor invoicing software, managing your cashflow has never been easier. Built for freelancers, sole traders, and small businesses, Debitoor grows with your company.

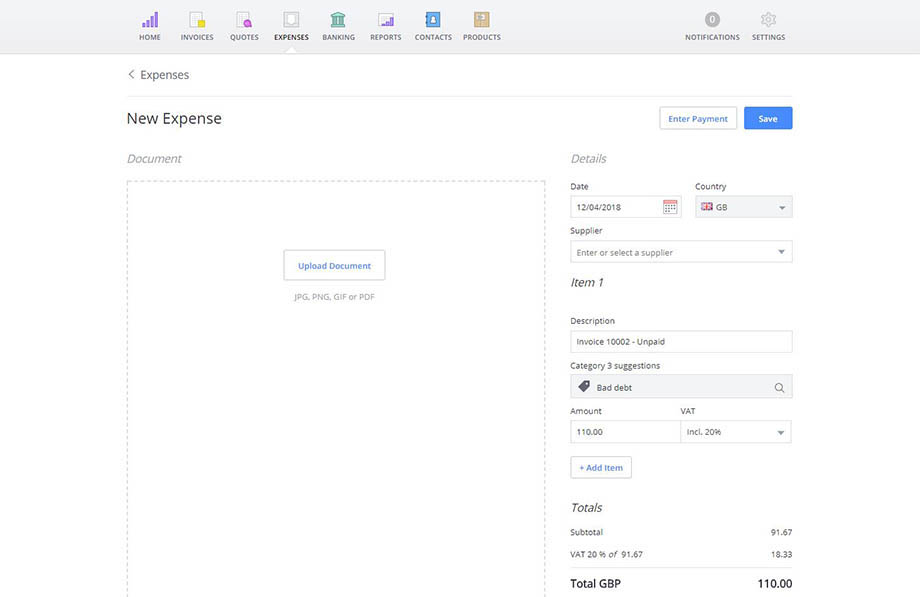

When you create an expense with Debitoor offers a ‘bad debt’ category for expenses, where you can record provisions for lost income. With our larger plans, you can also enter and track depreciation of assets.