7 online marketing metrics to apply to your business

When you start a business, it’s easy to focus on one main metric: your profits. However, there are some other important numbers that come from the marketing side of your business that can contribute to continued success.

This guide covers a series of different measurements that can be a big help to better understanding your business from the marketing perspective. Because they focus on the customer, they provide valuable insights into what’s working...and what could be improved.

Some of the metrics are available through your online accounting & invoicing software, but for others you will need web analytics basics to find the numbers to be used in a few simple calculations.

With that, we’re ready to take a look at 7 important metrics from digital marketing that will help give you a better grasp of both your customers and your business.

1. Check your profits at the end of each period

Yes, we’re talking about other important metrics, but at no point did we suggest that you ignore this one or that it was not important to your business. After all, it is a great indication of the financial health of your business.

If you’re not already keeping track of your income and expenses, it might be a bit of a task to determine revenues coming from your sales and what this means for profits.

Sales are an important part of running a business and often come with a cost to the business, so it’s important to understand how your cost of goods sold factors in when determining your profits.

If you find that your sales are taking off, it’s likely that you have a successful product/service that can lead to more customers, additional sales, and profit. If your profits are down, consider your costs and what can be done to boost sales.

2. Examine your customer conversion rate

Whether your business is e-commerce or is a brick and mortar shop, the end goal is for customers to make a purchase. A potential customer who makes a purchase has been converted to a customer.

The process for converting customers is different for every business. For example, a high street boutique depends in large part on their window display to initiate the first part of converting a customer. It has something that stands out and appeals to the customer, causing them to enter and take a closer look at a particular product.

If the size, colour, and price seem reasonable and it’s something that the customer enjoys/needs, they’re more likely to make the purchase. Of course, some businesses require a bit more aggressive marketing strategy, but in the end the browse versus purchase rate can tell you about your conversion.

A high conversion rate means that your customer has had a positive first experience and is more likely to return. A low conversion rate means their expectations were not met and it might be a reason to take a closer look at why this might be happening.

Being able to pinpoint where the customer was lost will better allow you to iron out the path to improved conversion rates. If a customer already showed interest, could you follow up with a newsletter, for example, that might remind them to make a purchase?

If you seem to have little interest from customers, find out why. There is a reason that there are so many surveys today. Customer feedback is one of the most direct ways to get to the root of an issue and start making improvements.

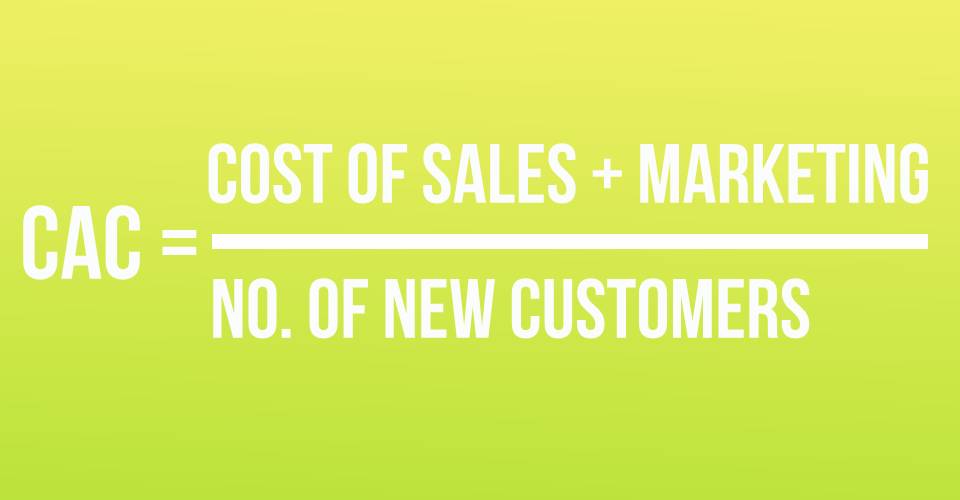

3. Determine how much it costs you to acquire a customer

That’s right, customers cost your business money. While they are typically one of the main sources of profit, they also all have a price. It’s an investment for that shop to set up an attractive window display. It’s important to understand the price paid for each customer that comes through your doors or visits your webshop.

This metric is known as the Customer Acquisition Cost (CAC). Essential for web-based businesses, it provides a clear indication of what each customer costs the company to acquire. This is important for understanding a business’ profitability.

To make it a little clearer, let’s use an example. Stephanie runs a yoga studio in Birmingham. She decides to place an ad on Google so that every time someone searches for a yoga studio in Birmingham, her studio will appear in the results as an ad at the top.

Let’s say she spends £600 for her ad to appear in the top results for 2 weeks. In those two weeks, she receives requests for information from 150 people. In the end, 32 of those signed up for a class. She can say that, for each new student from this campaign, she paid £18.75 (600 / 32).

CAC is an incredibly useful and informative metric that can be applied across your business including: to employees, shop window displays, website sales, etc.

4. Keep an eye on customer retention

In other words, are your customers leaving? If you’re constantly gaining new customers, it can seem like everything is going great, but you could be overlooking something important: customers who leave. In marketing terms, this is known as ‘churn’.

Ideally, customers stick with you and keep coming back. Repeat business is great for business but customer churn is an inevitable part of a business. How much, however, can be a major indicator of success.

Churn is generally a simple percentage calculation that gives you an idea of how many customers are leaving your business. For example, the churn rate of a subscription-based business would be determined by dividing the total number of subscribers lost in a given period by the total number of new subscribers at the beginning of the same period.

If you gain a total of 1,000 new customers at the beginning of March. Over the course of the month, you lose 50 (they cancel their subscription). Your business would then have a churn rate of 0.05%.

This is considered a low churn rate. However, if you find that your churn rate seems unexpectedly high, or if it continues to increase from period to period, it is likely time to take stock of your business and determine whether a new strategy is necessary.

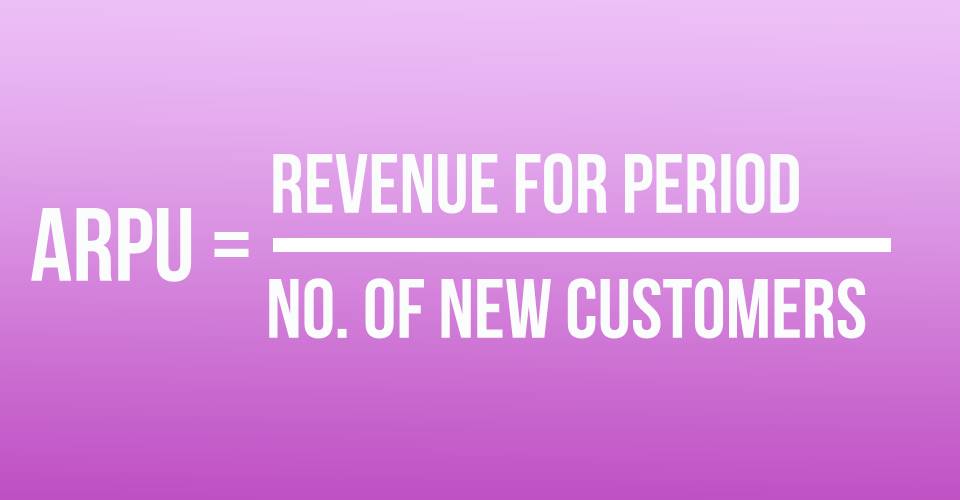

5. Predict the benefit of customers that stay

We’ve already taken a look at what acquiring a customer can cost your business, as well as how to calculate a percentage for those who leave. So what about the customers that stick around?

Now we get to the important part. How much are customers bringing into your business? There are two relevant metrics that are important for determining the revenue produced by one customer: the ARPU (Average Revenue Per User), and the future potential benefit provided by a customer: the CLTV (Customer Lifetime Value).

ARPU allows you to determine how much revenue customers bring to your business. Whereas the CLTV gives you tools to help determine how much your customers will contribute to future revenue.

To calculate this metric, it’s important to have already determined how often customers make a purchase on average, the average they spend at each purchase, as well as the average length of time they will continue to be a customer.

The CLTV equation is one that provides insight into how well customers are responding to a business. Repeat customers are considerably cheaper than new customers, so retaining customers can also have a big impact on a business’ profitability over time.

6. Analyse your return on investment and payback period

For most businesses, it’s important to understand if your money is being invested in the right places. The return on investment (ROI) and payback period metrics address these questions by allowing calculation of how well a particular campaign is doing, for example.

For example, if you were to invest £500 for an ad on Facebook, it is likely that you would want to determine whether any money was made from this campaign in order to measure its effectiveness.

If the business receives 20 new customers from the campaign, and in total there is £650 in new orders from these customers. This data can be used to determine the ROI for the Facebook ad campaign: (650 - 500) / 500 = 0.3 or 30%.

While this result is positive, ROIs can be negative, which would likely indicate an unsuccessful campaign in which money was lost. However, this also might mean that the cost of acquiring a customer is higher than their first purchase. Customers with a long lifetime will contribute more over time.

The amount of time it takes for a customer to pay back the amount that the business spent to obtain them is known as the ‘payback period’. To calculate this, multiply the ARPU by the gross net profit. For example, if your profit margin is 62% and ARPU is £10, the payback period will be 6.2 months.

7. Don’t jump to conclusions about your metrics

There might seem like a lot of numbers and calculations that need to be covered, which might be a bit intimidating at first. However, they all provide a range of helpful measurements for helping to grow a business and avoid common pitfalls.

While every business aims to make a profit, the numbers you want to see might not appear in the first few months or even years, so it can be useful to track growth and make necessary adjustments over time.

Just because the numbers might show a less than desirable result does not mean that a different one isn’t possible. Take the time to examine the metrics and look to where changes can be made.