Invoicing software not only lets you create and send invoices, but it also helps you manage accounting aspects of your business such as the depreciation of assets. In this article, I will explain what depreciation means, and how to record it with your invoicing software.

What are assets?

An asset is any item of value owned by a company or individual. There are several types of assets including fixed assets, tangible assets, intangible assets, and current assets. In the case of depreciation, we will only focus on fixed assets.

A fixed asset is an asset that cannot be easily converted into cash, and is not expected to be sold within the first year of use. Fixed assets are generally long-term larger investments for a business, such as a patent, a company car, or office equipment.

Fixed assets can fall under the categories of tangible and intangible, meaning that the asset either has a clear purchase value and is used to produce goods and services (e.g. machinery), or it is a non-physical asset that helps a business generate income (e.g. a patent).

Fixed assets are important to a business as it contributes to the financial value of the company. Investors also use this information when assessing the potential of your company.

When measuring the value of a fixed asset, the depreciation must be taken into account.

What is depreciation?

Depreciation is the loss in value, quality, or quantity of a fixed asset over time. The value of an asset reduces (depreciates), as it ages, the more it is used, or as technology advances and new models are established.

Calculating the depreciation of assets is a useful tool for many businesses, as it allows them to recover the asset’s cost over its lifespan rather than immediately recovering the cost at the time of purchase.

There are several types of depreciation methods, such as accelerated depreciation, reducing balance depreciation, and units of production depreciation, but in this article, we will focus on straight-line depreciation.

Straight-line depreciation refers to the method of spreading the total cost of the asset evenly throughout each year it is useful to the company.

To calculate the straight-line depreciation, you will need to estimate the assets useful life and residual value.

The useful life refers to the amount of time (measured in years) that the asset will be functional and useful to the company.

The residual value is an estimate of how much the asset will be worth at the end of its useful life when it is no longer useful to the company.

How do you calculate straight-line depreciation?

To calculate the straight-line depreciation, you take the original cost of the asset, minus the residual value, then divide by the useful life.

(original cost - residual value) ÷ useful life

For instance, let’s say you purchased a piece of machinery for your business that cost £10,000. You estimate that the useful life is 10 years, and after 10 years, it will be worth £2,000 (residual value). From that information, you can calculate the depreciation:

(£10,000 - £2,000) ÷ 10 years = 800

From this calculation, every year, the machinery loses £800 in value.

How do I record depreciation on my invoicing software?

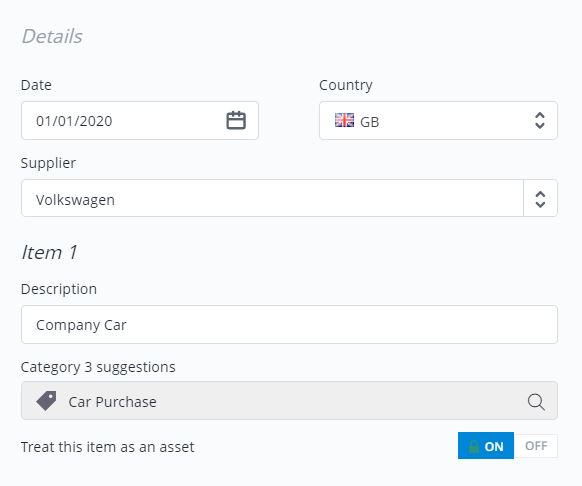

With invoicing software, you can easily record your expenses and mark them as assets. With Debitoor, you can quickly calculate the straight-line depreciation by following these steps. In this example, we will show you the depreciation of a company car purchase.

First, log in and go to the ‘Expenses’ tab. Create a new expense, and input the details. Choose from one of the many expense categories, and select ‘treat this item as an asset’.

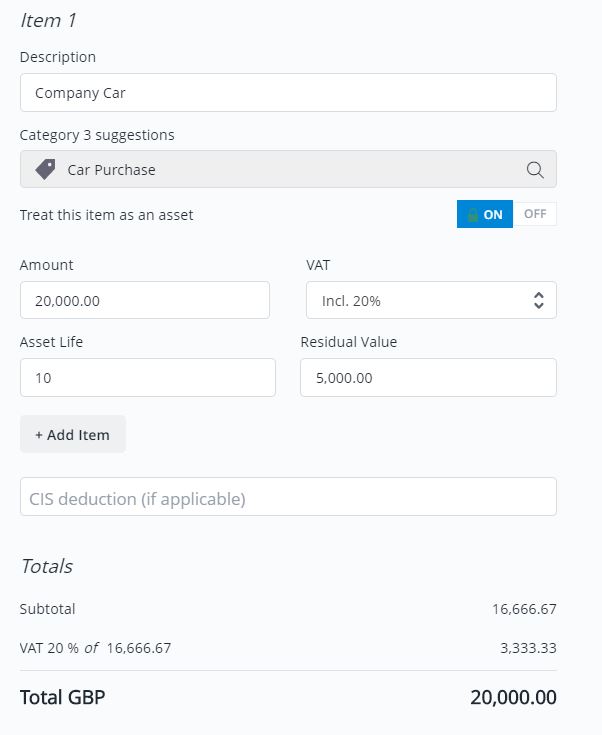

Next, you can enter the amount you paid for the asset, the asset life (in years), and estimated residual value (in GBP).

You can enter an optional document such as an invoice or receipt, and click ‘Save’. Once the asset is saved, you can view the straight-line depreciation at the bottom of the expense page.

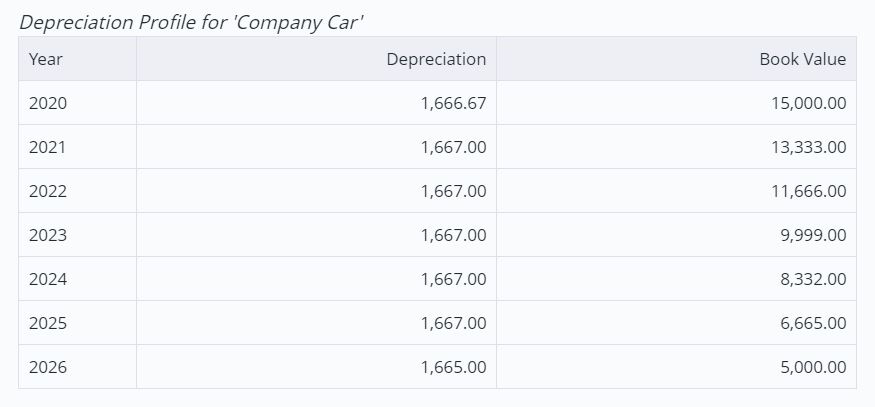

Debitoor will do all of the calculations for you based on the information you provided. In the chart, the depreciation column indicates how much the value of the asset decreases in that year. The book value indicates the value of the asset at the end of that year as shown on the balance sheet.

You may see that the depreciation values differ from the first and last year, as this is calculated by the date in which you purchased the asset. If you purchased it midway through the accounting year, the first and last depreciation value may be lower than the rest of the years.

If you want to delve deeper into this topic, you can check out our small business guide on assets, depreciation and amortisation. If you want to test it out, feel free to sign up to our 7-day free trial.