Have you heard about workplace pensions but unsure of exactly what they are? Don’t worry, pensions can certainly be a confusing topic. In the UK, employers must offer a workplace pension to employees, and automatic enrollment for eligible staff.

In this article, I will explain everything you need to know about workplace pensions both on the employee and employer side.

What is a workplace pension?

A workplace pension is a type of pension that is set up through your employer. It is a scheme to help you save money for retirement by making contributions that are automatically deducted from your salary or wages.

In a workplace pension, the employer will also contribute a percentage along with the amount being deducted from your pay.

Workplace pensions may also be referred to as a ‘work-based’, ‘occupational’, or ‘company’ pension scheme.

How to set up a workplace pension as an employer

All employers in the UK are required to set up a workplace pension scheme. To do so, you will need to contact a pension provider. There are several in the UK, but the main two are NEST and Aviva.

Once you have set up your account with the pension provider, you will need to determine which employees are eligible for automatic enrolment.

If an employee is 22 years or older, and makes at least £833 per month / £10,000 per year, they will need to be enrolled in the scheme and start paying towards their pension. The employee is able to opt-out at any time.

How much do I contribute to a workplace pension?

The minimum amount you can contribute to your workplace pension each month is 8%. Of that 8%, 5% is the employee contribution, and 3% is the employer contribution.

Both the employer and employee can decide to contribute more than the minimum of 3% and 5% at any time.

If the employee decides to opt-out of the scheme for whatever reason, then the employer is also not required to pay into the pension.

What is the difference between a workplace pension and a state pension?

A state pension is organised by the UK government and paid out when you reach the state pension age which is currently 65 (2020). You will need to have at least 10 years (consecutive or not consecutive) of paying UK national insurance to qualify for the state pension.

A workplace pension, on the other hand, is set up by your employer, and both the employee and employer contribute a percentage of each pay to your pension account. The money is owned by the employee, rather than issued by the government and the earliest you can start taking your workplace pension is when you reach the age of 55.

A state pension is usually paid by the younger generations National Insurance contributions, so the younger generation is essentially paying for the older generations pension.

A workplace pension is paid out from the money both the contributed to the account during the employees time of employment.

What is the difference between a workplace pension and a personal pension?

The main difference between a workplace pension and a personal pension is the amount of control the employee has over the money in their pension account.

In general, the money put in a pension account is invested. In a workplace pension, the pension provider decides how your money is invested, whereas in a personal pension, the account holder can make the investment decisions.

Another difference is who is eligible to contribute to your pension. With a workplace pension, only the employee and the employer can make contributions. With a personal pension, it is usually just the employee/account holder. However, an employer, and any other person (e.g. spouse, family member, friend, business partner), can also contribute to your personal pension.

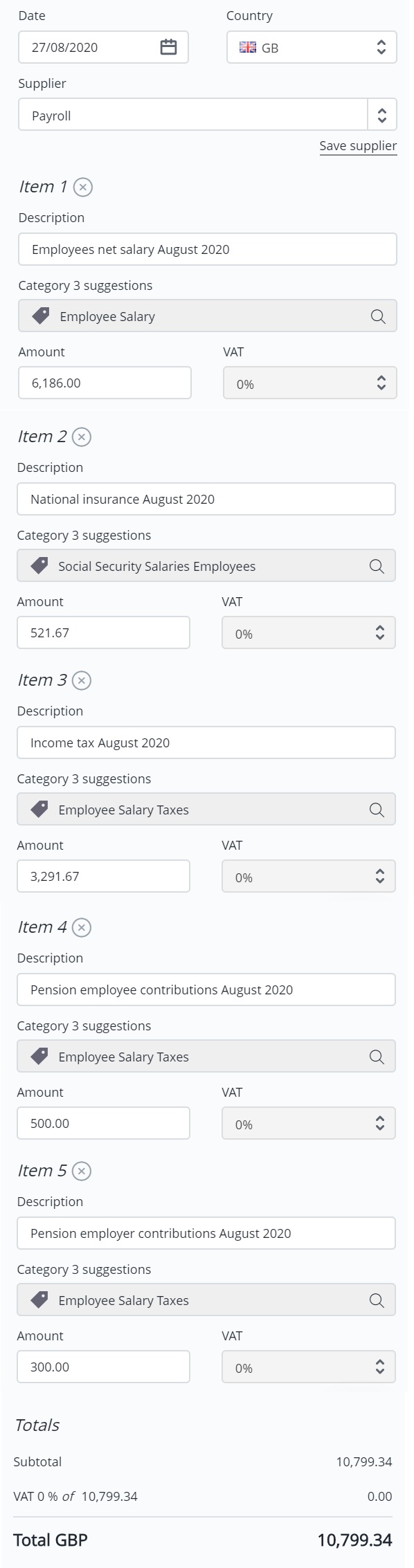

How do I record pension contributions in my invoicing software?

Invoicing software not only helps you create and send invoices to your clients, but it also helps you record expenses such as payroll and pension contributions.

With Debitoor, you can add separate lines to your payroll expense to break down the different deductions including income tax, national insurance contributions, and pension contributions.

Here is an example of how you can enter your payroll and pension information on Debitoor:

To make your life easier, we suggest that you enter one payroll expense for all employees rather than a separate expense for each employee.

On Debitoor, you can choose from one of our many expense categories to keep track of how much you are spending on each payroll category each month.

There is no limit to the amount you can have saved in a pension. You are able to have both a personal pension, and a workplace pension, and still qualify for the state pension.

If you need more information regarding UK workplace pensions, I would suggest contacting a pension provider, or going to the UK Government website.