Balance sheets are often one of the most important financial statements used by business owners, accountants, investors, and other stakeholders.

Financial statements are merely a written record of a business’s position and their financial activity. These statements are made up of a number of standard reports, with the balance sheet being a major one, other additional reports include the income statement, statement of cash flow, and statement of retained earnings.

So, what IS a balance sheet?

The balance sheet is a written report that shows insight into what a company owns (assets), what they owe (liabilities) and how much money their owners and shareholders have invested into the business (stockholders equity).

This brings me to the next point: the name itself. The reason we call this the “balance sheet” is quite obviously because, well, it should balance.

The first (and probably only) equation you need to know for the balance sheet is the following: Assets = Liabilities + Stockholders Equity

The balance sheet is designed to list all assets on the left hand side, and all liabilities and stockholders equity on the right hand side.

The balance sheet is formed by using a double entry bookkeeping system, where all transactions are recorded in at least two different accounts. This means that every transaction has a corresponding positive and negative entry. In other words, each entry has a corresponding debit and credit.

The reason for this is that once you have recorded all transactions and are now drawing up the balance sheet, the value of your total assets should ultimately be equal to to the total sum of your liabilities and stockholders equity, hence, it should balance!

If the equation A = L + SE does not end up balancing, then this means you have probably done something wrong in the recordings of one or more transactions.

Contents and format of the balance sheet

The balance sheet shows the financial position of a business at a given point in time. It can be prepared at any time, although it is most often prepared at the end of each accounting year.

The balance sheet is split into three different sections, assets, liabilities, and stockholders equity. These sections can then be further split into current and noncurrent assets, and short-term and long-term liabilities, for example.

What you list under each of the three categories (assets, liabilities, and stockholders equity) will vary from business to business depending on the industry you are operating in. But do not worry, will discuss each section below, to make sure you understand the fundamental basics of the balance sheet.

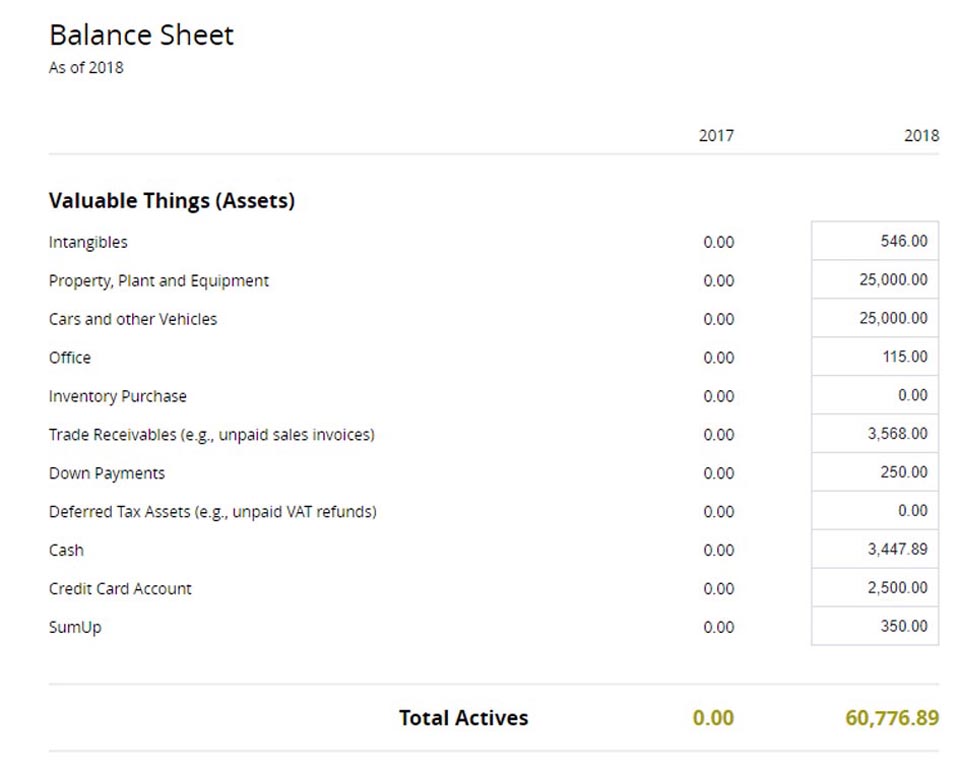

Assets

Assets shown on the balance sheet represent items which a business owns, that hold value. Assets can be split into current, and noncurrent categories. The reason for this is to show the level of ease relative to liquidation.

Liquidity is determined by how quickly and easily you can convert assets into cash. For that reason, cash itself is considered the most liquid of all assets. Noncurrent assets such as buildings and land are less liquid because they do not have the same capability of being quickly converted into a current asset such as cash (since it is unlikely that they will sell overnight).

Current assets Current assets are assets that can be converted into cash within one year. Some examples of current assets include:

- Cash

- Accounts receivable

- Other current tangible assets

Noncurrent assets Noncurrent assets are assets which are not expected to be converted into cash within one year. Some example of noncurrent assets include:

- Buildings

- Land

- Machinery

- Equipment

- Intangible assets

The total assets shows a representation of the sum of both current and noncurrent assets.

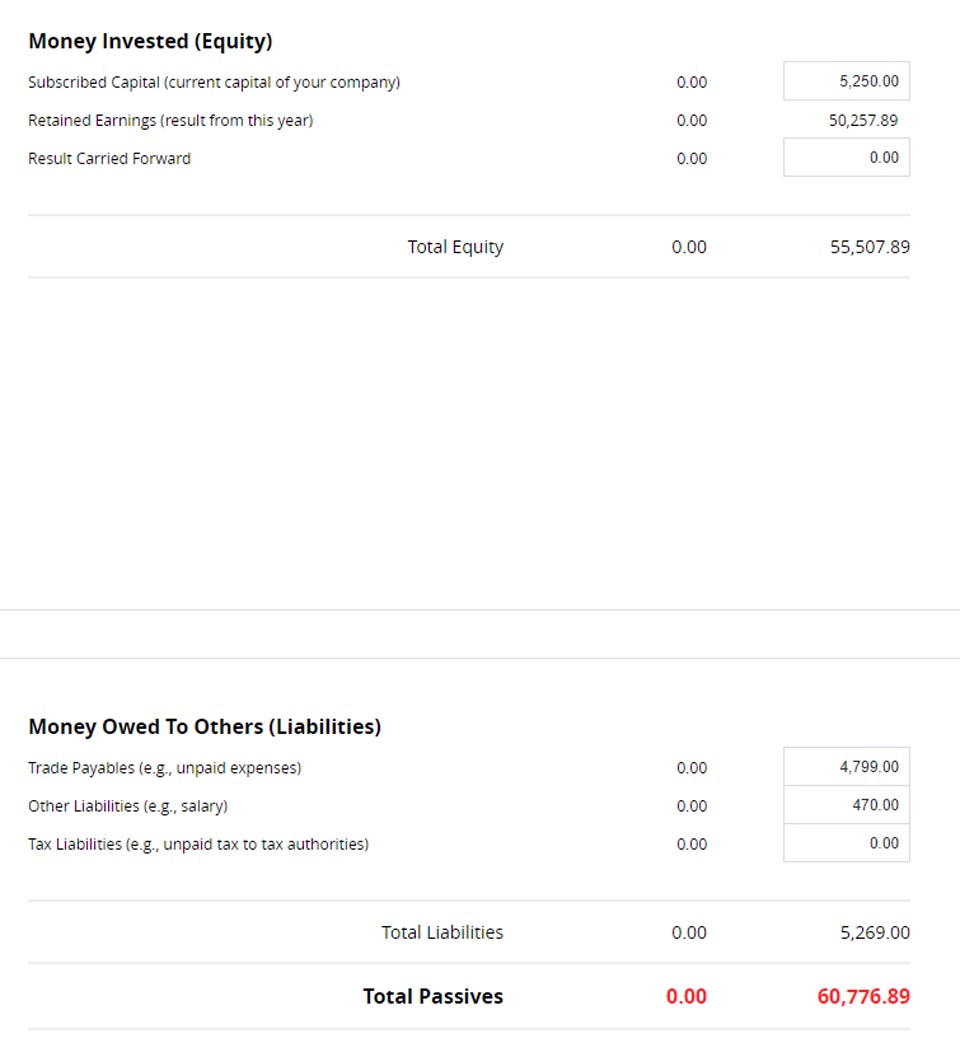

Liabilities

Liabilities are something which a business owes, such as debts or obligations. Just like assets, liabilities can also be long and short term.

Long term liabilities Long term liabilities are all debts or obligations owed by the business that is expected to have a payment period of more than one year. Some long term liabilities include:

- Mortgage bond

- Long term loans

- Pension liabilities

Short term liabilities Short term (or current) liabilities are all liabilities owed to creditors that the business expects to pay within one year. Some short term liabilities include:

- Wages payable

- Accrued expenses

- Short term debt

- Dividends payable

The total liabilities shows a representation of the sum of both long and short term liabilities.

Stockholders equity

Stockholders equity, also known as owners equity or shareholders equity, is comprised of the initial capital invested into the business, together with any other retained earnings that have been reinvested in the business. Stockholders equity can also be calculated by taking your total assets minus your total liabilities (simply rearranging the A = L + SE equation, to be A - L = SE).

Balancing the balance sheet

Once you have entered each transaction correctly into your [general ledger[(/dictionary/general-ledger), and identified which assets or liabilities can be classified as long or short term, then you can draw up a clean and neat balance sheet for your business.

If you have recorded everything just as it should be, then you should find in your balance sheet that the value of your total assets will be equal to the sum of the total liabilities and stockholders equity.

For any business, a balance sheet is a useful tool to give insights into the financial condition and health of a business. It gives an indication of what a business owns, how much they expect to bring in and how much they expect to pay out. Keep in mind that the balance sheet is a snapshot of the financial state of a business, only at a given point in time.

Financial statements are an important tool to measure the position and status of your business, for both internal and external parties. As a business owner, it is so important that your accounting records are accurate and true.

When you use an accounting and invoicing software such as Debitoor, you can easily and instantly generate financial statements. This can save you both the time and effort it would take when drawing up each statement manually.