Launching a small business often takes up a lot of time. And money. For many businesses just starting out, a loan can make sense. Loans can provide that little extra capital that is necessary to really get things off the ground, and often, favourable terms can be found.

But getting a loan also includes an added level of management from an accounting point of view. It’s one thing to receive the money, and make payments, but how do you ensure this appears correctly in your accounts and is reflected in your financial reports?

Accounting & invoicing software can provide a solution for managing these balances and regular payments.

Including a loan in your bank account

In Debitoor, it is possible to include a loan in the accounting side. There are just a few steps to get it set up and then you can set it up to manage your loan and payments made towards it within your account. Keep in mind that with Debitoor, no money is actually handled, it is a means for you to manage the numbers only.

Step 1: upload your bank statement

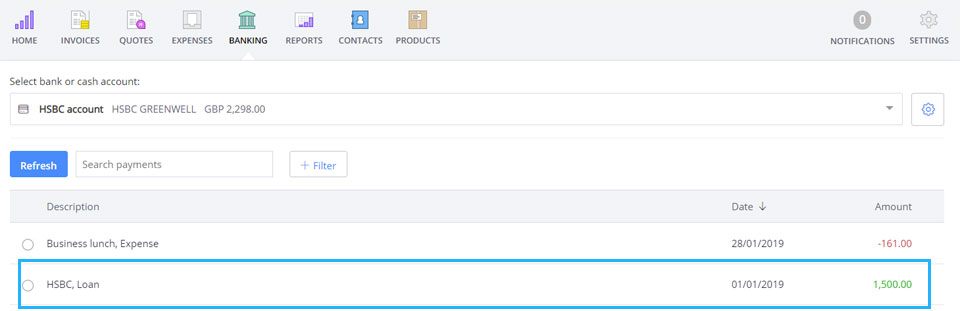

The first step will likely be that you receive the money from the lender. This will appear as a positive payment into a business bank account. In Debitoor, if you’re using the automatic bank reconciliation function to upload your bank statements, the loan amount will be included on your statement and will appear as a positive balance in the account to which you upload it in Debitoor:

Step 2: create a 0 balance manual bank account for your loan

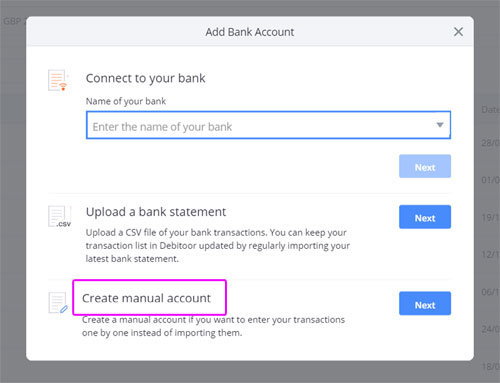

The next step is to create the loan account. In your ‘Banking’ tab, click on the dropdown menu and click the ‘New account’ button.

When you see the following window, select the third option: ‘Manual account’.

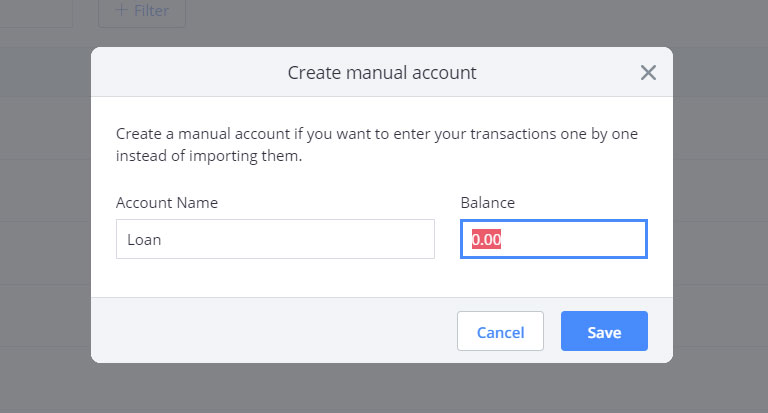

You can name this account ‘Loan’ or ‘Small business loan’, for example. This is for your own reference within your account.

Leave the balance of the account as ‘0.00’. We will adjust this in the next step.

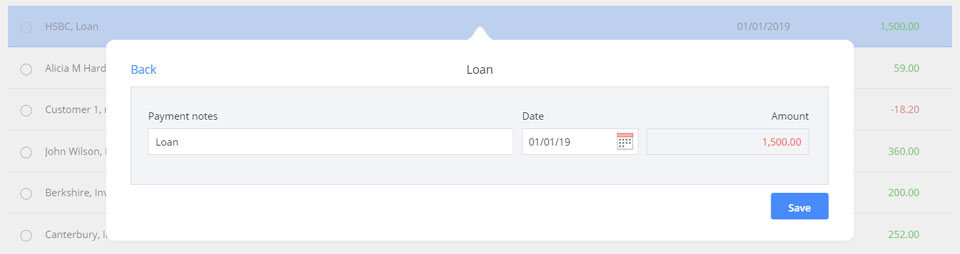

Step 3: mark your loan as a transfer from your Loan account

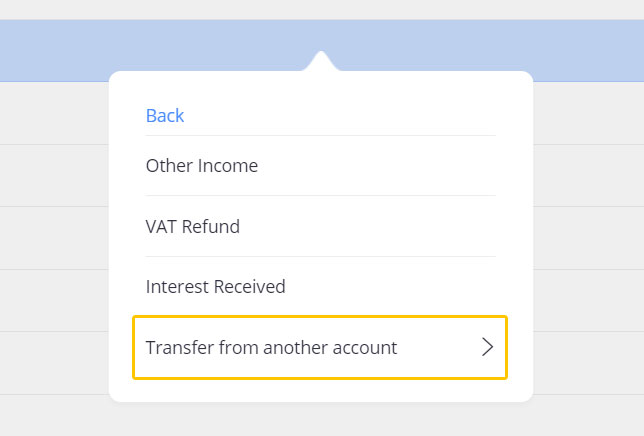

In this step, return to the bank account to which you uploaded the bank statement that included the loan amount. Find the loan amount in the list and click on the line. You will see a menu for marking this amount - select ‘More’ and choose the last option ‘Transfer from another account’. Select the loan account you created in the previous step.

This will automatically add the full amount in the negative to your loan account. It will also allow you to make payments to the account.

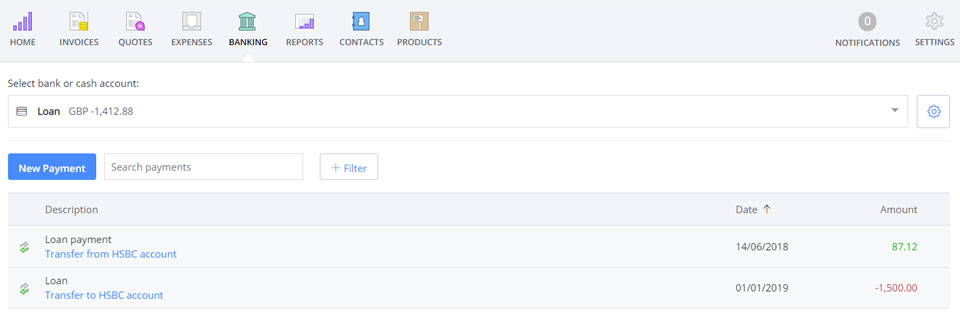

Step 4: transfer payments from your bank uploads to your loan account

Once you have a negative balance in the loan account you created, you can update the balance by transferring payments made from your bank account that appear on your statement upload. When you transfer a payment from your bank account to your loan account, you can also adjust the description, if necessary.

As you continue making payments, your loan balance will return to 0. This allows you to keep track of your loan and ensure that it appears properly in your Debitoor account.