Small businesses today have many options to expand and grow. This often means a customer base that is located outside the country in which your business is based. This brings a new set of added complexities, but they’re easily navigable with the right software.

Creating invoices in foreign currencies is one of the many ways that using online invoice software like Debitoor can simplify the billing process. But as easy as it is to create an invoice in another language or currency, you might be asking - what about the payment side?

This article will help clarify how to manage payments with exchange rate differences for invoices in foreign currencies in your Debitoor account.

Currency exchange rates

When you create an invoice in, for example, Euros, if your business is based in the UK, you’ll find an option in the invoice form to add in the current exchange rate. Exchange rates fluctuate regularly, and this often affects both income and expenses if you’re working across borders.

The difference between your business base currency and a foreign currency on an invoice can result in either a gain or loss to the business. In other words, after determining the exchange rate, the business might receive more or less money than specified on the invoice.

When a business receives more money than the total on the invoice, this is considered an exchange gain. When the amount is less than that specified on the invoice, it is known as an exchange loss.

Example of an exchange difference

An example can better illustrate what the exchange difference means when managing payments:

A UK-based business invoices a Belgium-based customer for €55. On the day that the invoice is created and issued, the exchange rate is: €1 = £1. The customer does not pay immediately, so the exchange rate continues to fluctuate.

On the day the customer pays the invoice, the exchange rate is: €1 = £0.75. The exchange rate changed as the Euro depreciated. However, the amount specified on the invoice is still the same amount paid, so the customer pays the €55.

On the day of issuing the invoice, this payment would have meant £55, however, on the date of payment, €55 will come to £41.25. In this case, the business faces an exchange loss.

Record a currency exchange difference in Debitoor

Depending on your subscription and how you manage your payments, there are two ways to handle incoming payments that involve exchange rate differences:

- Adding a payment manually from your Cash account, or

- Uploading a bank statement for bank reconciliation to use the matching feature

1. Recording payment from the cash account

Recording exchange gains and losses for invoice payments is easily done in Debitoor by following the steps below:

Exchange losses and invoice payments

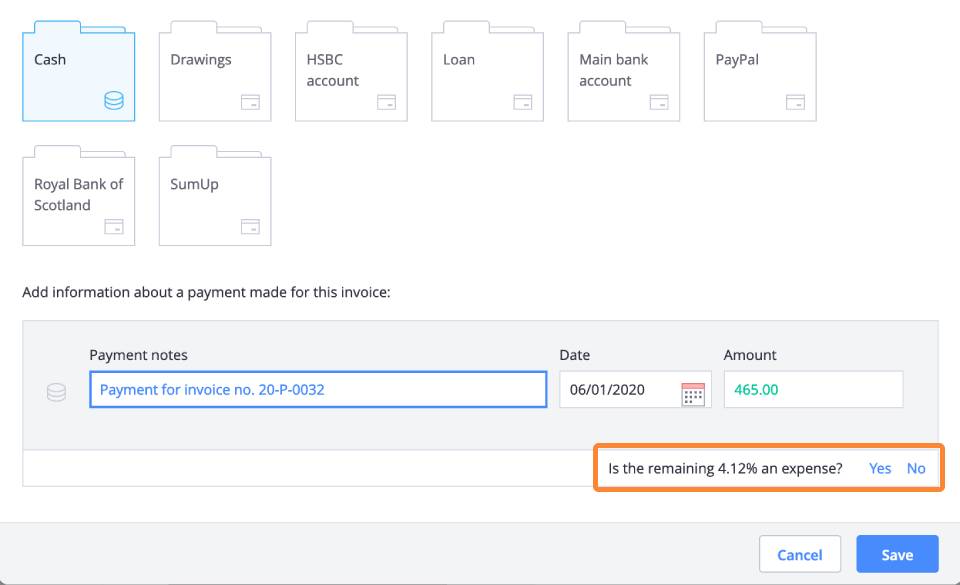

From your Invoices tab, select the invoice to be paid from your list. When you click on that invoice, you’ll find the ‘Enter payment’ option at the top right. A window will appear where you can enter the amount received and provide a description, if necessary.

By default, Debitoor will suggest the total amount in GBP even if the invoice was issued in Euros. You can adjust this amount if necessary.

As this is an entry with an exchange loss, the amount entered will be less than the total amount for which the invoice was issued. After entering the amount (or if the default is accurate), click anywhere else within the window.

You’ll see a small blue text appear under the amount. This is the difference between the invoice total and the amount entered, which the software will detect automatically and offer the option of marking it as an expense.

‘Is the remaining __% an expense?’. If it is for a currency exchange difference, click ‘Yes’. You’ll then be able to specify the category of the expense - in this case, ‘Financial Adjustments’.

An expense for the amount of the exchange loss will automatically be created, and the invoice will be marked as ‘Paid’.

Exchange gains and invoice payments

When the exchange rate causes the amount paid by the customer to be more than the total as stated on the invoice, this is an exchange gain.

Handling this type of currency exchange difference in Debitoor starts the same: click ‘Enter payment’ from the invoice that has been paid. Because it isn’t possible to enter an amount greater than the total of the invoice, click ‘Save’.

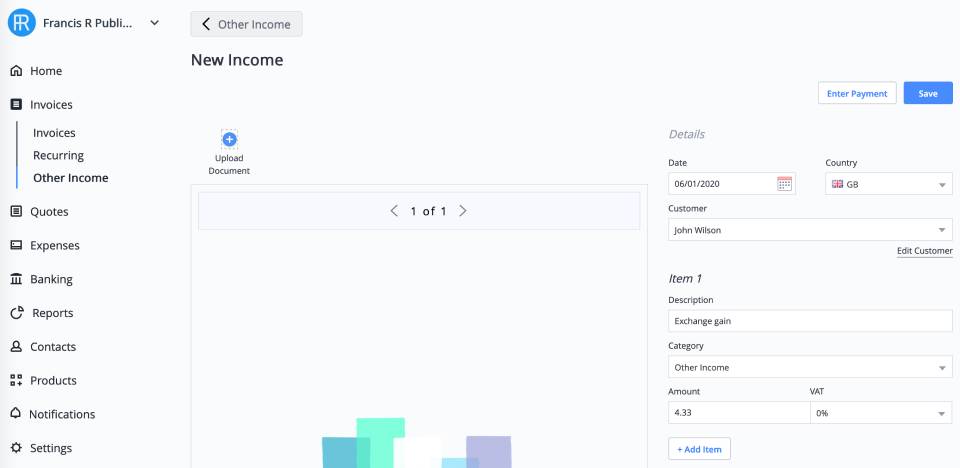

The next step takes a bit of calculation, but is quick and easy. Determine the exchange gain amount and record it as ‘Other Income’. To do so, plug the numbers in to the following equation:

Amount received - Amount invoiced = Exchange gain

In your ‘Invoices’ tab, click ‘Other Income’ and click ‘New Income’. Enter the customer who made the payment, the date, etc. and then a description of the source of the income, likely something such as “Exchange gain”.

2. Recording exchange differences with bank reconciliation

If you upload your bank statements to your Debitoor account, the process for managing exchange gains and losses is a little different. When you add a bank account and upload your statements, the automatic bank reconciliation function will match invoices with payments based on the total amount and date.

Because this gets a bit more complicated with currency differences, it likely won’t happen automatically, but is still a swift and simple process.

Automatic bank reconciliation and exchange losses

Just like the first steps above, first find your invoice from your invoice list and click ‘Enter payment’, selecting the bank account and corresponding payment. Alternatively, you can enter payments from the account in the ‘Banking’ tab. By clicking on a payment, you’ll see the option to choose ‘Payment for an invoice’ where you’ll see the top invoices suggested based on the payment.

Select the invoice and if the amount received is less than the amount stated on the invoice, you will see blue text asking whether the remaining amount is an expense. Click ‘Yes’ and select the ‘Financial Adjustments’ category for your expense. The expense will be created, and the invoice marked as ‘Paid’.

Automatic matching and currency exchange gains

For cases involving currency exchange gains, the payment should be entered on the invoice, either by selecting the payment from the invoice after clicking ‘Enter payment’, or through the ‘Banking’ tab by selecting ‘Payment for an invoice’ after clicking on the payment itself.

Because an amount higher than the total cannot be entered on an invoice, it will be necessary to record the remaining amount as ‘Other Income’. In the ‘Banking’ tab click on the remaining amount, click ‘More’ then select ‘Other Income’ to record this amount.