Now available in Debitoor: the flat rate scheme! Find out more about the flat rate VAT scheme and how it works in Debitoor:

Running a small business in the UK, there are many things to consider, to calculate, to evaluate. Once your business is over the VAT threshold, tax is one thing that is unavoidable. While it can cause headaches, there are easier ways to stay on top of tax and make your quarterly reporting (even under HMRC’s Making Tax Digital), just a little bit easier.

A brief introduction to the flat-rate scheme

Introduced in the 2002 budget, the flat rate scheme was developed by HMRC with the aim to help out small businesses in the UK. It does this by providing some relief when it comes to dealing with VAT returns.

Initially, it was also a good option for small businesses looking for an increase in revenues because it generally meant a lower VAT rate than they would then be charging their customers, which translated to a difference that could be kept by the business. However, this changed in 2017 when HMRC introduced a higher 16.5% rate to combat this type of alleged abuse of the flat-rate scheme.

What makes the flat rate scheme different

The flat rate scheme allows a business to pay a fixed rate of tax to HMRC. The rates start as low as 4% if your business is in food retail, children’s clothing, newspapers, confectionary, or tobacco.

The rates go up to 14.5% for businesses such as accountancy & bookkeeping, IT consulting, lawyers, legal services, architects & structural engineers, for example. Other businesses fall on a range between these two rates. Take a look at HMRC’s page on flat rates for business type.

The 16.5% rate applies to businesses that are considered ‘limited cost’ business. A business will fall into this category if it meets the cost of purchasing goods is:

Less than 2% of your annual turnover, or Less than £1,000 per year (if they are above 2%)

These rates are compared to the 20% rate that would be paid on the Standard VAT Accounting Scheme.

Advantages & disadvantages of the flat-rate scheme

While it can seem like an obvious advantage to pay a flat-rate that is likely a fair amount less than you would pay on the Standard VAT Accounting Scheme and you get to keep the difference between what you charge your customers and what you pay to HMRC, there is one distinct disadvantage: you are not able to claim VAT you pay out in your business.

This means that any VAT you pay on your purchases can not be reclaimed when it comes time to file your taxes. While you won’t have to bother with your receipts, it will not exempt you from paying VAT and it does prevent you from claiming it.

Is the flat rate scheme right for your business?

The flat rate scheme aims to offer a clear advantage: a reduced amount of time spent on your accounts due to a simplified, flat payment rate and the elimination of claiming VAT on expenses.

However, your business does need to be eligible for the flat rate scheme in order for you to join. To be eligible, your business should:

- Be VAT registered

- Have an expected taxable turnover under £150,000 excluding VAT in the next 12 months

In your first year after joining the scheme, you’ll benefit from an additional 1% discount. If on your 1 year anniversary of joining the flat rate scheme your business has passed a taxable turnover of £230,000 or expects to in the next 12 months, you will need to leave the flat rate scheme.

If your business is no longer eligible, you will be required to leave the scheme. Many businesses also leave the scheme if their taxable turnover falls below the VAT registration threshold of £85,000.

Making the decision to join the flat rate scheme if your business is eligible is entirely up to you. One thing that is commonly suggested as far as determining whether the flat rate scheme could be useful for your business is to calculate whether the monthly VAT your business spends on expenses is more or less than the VAT that you collect from customers.

You should also consider the growth rate of your business - if it’s growing rapidly, does it make sense to join the flat rate scheme if you will no longer be eligible next year?

The flat rate scheme and Making Tax Digital

With HMRC’s introduction of Making Tax Digital in April, 2019, businesses over the £85,000 VAT threshold will need to use approved accounting software to submit your VAT returns online directly to HMRC.

Businesses that fall under the MTD requirements will need to sign up and connect with their accounting software. Different VAT schemes can be used with MTD, including the flat rate scheme.

Submitting your flat rate scheme VAT return to HMRC

Using making tax digital software to record your VAT is required by HMRC if your business is over the threshold. This includes businesses on the flat rate scheme, so it’s important to be sure that your accounting software offers the flat rate scheme.

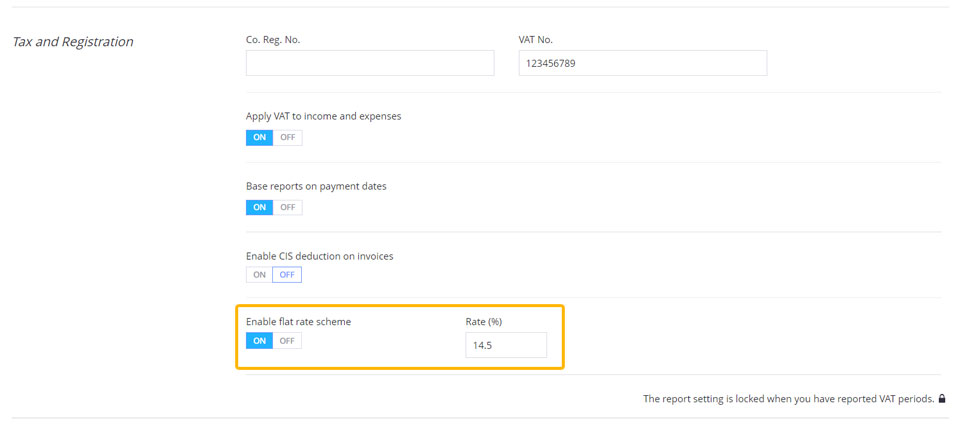

Debitoor now offers the flat rate VAT scheme. It takes just the simple click of a button to enable it within your account. Enter your VAT rate and it automatically applies it to your VAT return, making it simple and fast to submit directly to HMRC.

You’ll find it within your account by clicking ‘Settings’ at the top right, then ‘Settings’ and scrolling down to the ‘Tax & Registration’ section.