For anyone running a small business, it’s important to have the right tools for creating invoices, sending quotes, and keeping track of your company finances. When looking for software to help you do this, you’ll come across many different options for invoicing and accounting, but, rather than having one program for your invoices and one program for your accounts, why not choose software that combines the two?

Depsite the name, Debitoor invoicing software isn't only designed for creating and sending invoices; with a range of features for bookkeeping and accounting, Debitoor can help small business owners take control of their finances. So here’s 5 ways you can use your invoicing software to manage your company’s accounts.

Managing assets and calculating depreciation

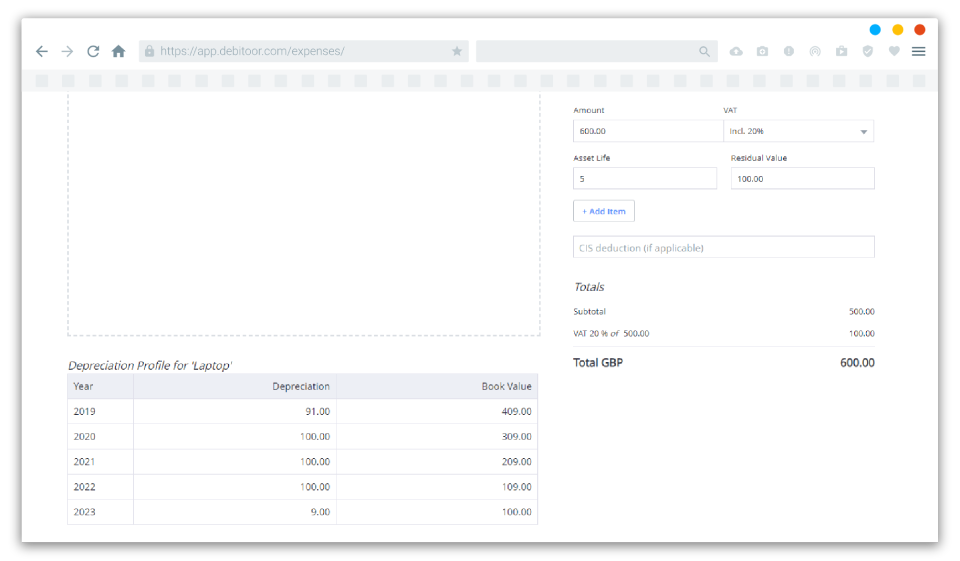

When you make purchases for your business, you’ll sometimes invest in fixed assets, which are are items that contribute to your company’s long-term operations. Because fixed assets add value to your company over an extended period of time, it’s important that your accounts reflect this. Rather than recording the entire cost as a single, one-off expense, the cost should be spread throughout the entire period that the asset adds value to your business. This process is known as depreciation.

There’s several different ways to calculate depreciation, some more complicated than others. Fortunately, you don’t need to do this yourself as Debitoor invoicing software lets you process expenses as assets and calculates depreciation automatically.

All you need to do is indicate that an expense is an asset, fill in how long you expect the asset to last, and record how much you think the asset will be worth when its no longer useful to you. Debitoor will then automatically create a depreciation expense each year until the asset is sold on or becomes obsolete.

Creating financial reports

There are many different financial reports that can be used to get an overview of your company’s finances, but two are particuarly important: the profit and loss statement and the balance sheet.

Firstly, the profit and loss statement, which is sometimes referred to as the income statement or P&L statement, shows a business’s revenue and losses over specific period of time and essentially helps you calculate whether your business is profitable. Secondly, the balance sheet, which outlines a company’s assets, liabilities, and equity, can be used to help you understand the liquidity and efficiency of your company's finances.

There's specific information that needs to be included on balance sheets and profit and loss statements, and it can be difficult to create these reports manually if you don't have a background in accounting. However, with invoicing and accounting software like Debitoor, even inexperienced business owners can generate financial statements with just a few clicks.

To find out more about how you can use financial reports for evaluating your financial year – and how you can do this with Debitoor – check out our blog post about reading reports and evaluating your year.

Submitting your VAT Return

If you run a UK-based, VAT-registered company, you’ve probably heard of HMRC’s Making Tax Digital initiative, which requires most VAT-registered businesses to report their VAT through authorised Making Tax Digital software.

From April 2019, Debitoor users will be able to create VAT reports and submit them directly to HMRC from their Debitoor account. Whenever you generate a VAT report, it will be based on the data you've entered for the selected period, so there’s no need to transfer data from one program to another.

Making Tax Digitial is quite a big change for businesses that are used to submitting their VAT Returns through HMRC's website, and its likely that you'll have a few questions. To get the answers you're looking for, check out our Q&A about Debitoor and HMRC's Making Tax Digitial.

And if you have a VAT-registered business that isn't based in the UK or isn't covered by the MTD initiative, you can still use Debitoor invoicing software to create VAT reports that help you manually submit your VAT Return.

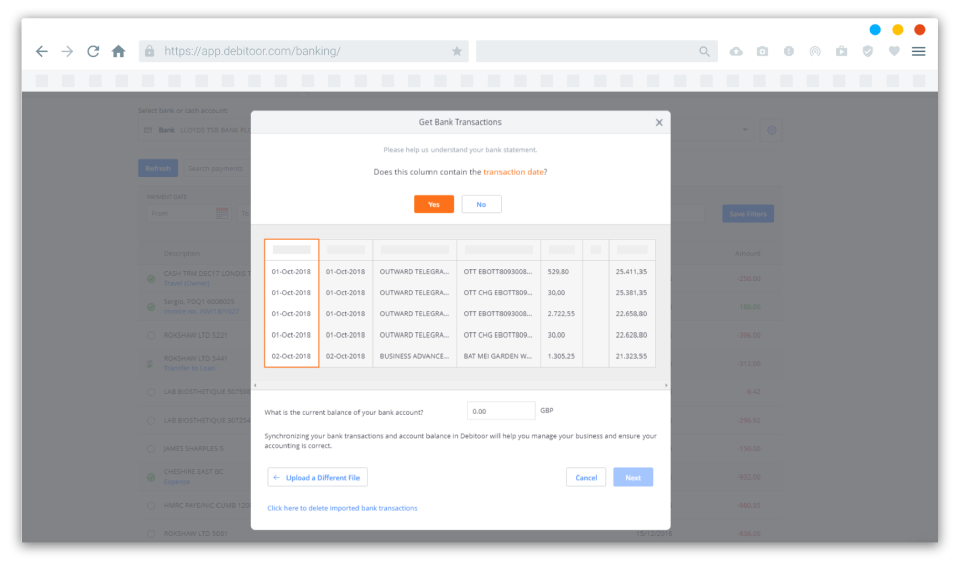

Reconciling your bank statements

Bank reconciliation is the process of matching the transactions in your business records with transactions from your bank records. We recently looked at why bank reconciliation is important for small businesses – primarily to prevent fraud and to resolve mistakes in your accounting records.

Bank reconciliation can be a long, tedious task if you try to do it manually, but with invoicing software like Debitoor, you can compare and match transactions in minutes. All you need to do is upload a .csv file – the software does the rest.

Working with your accountant

Invoicing software like Debitoor makes it easy for you to take charge of many different accounting and bookkeeping tasks, but there are times when you’ll still need the help and advice of a professional.

Traditionally, you would have to print all of your information and send your accountant physical documents. But this has a few different pitfalls: it's time-consuming, it's bad for the environment, and it runs the risk of documents becoming lost or damaged.

For an easier way to collaborate with your financial adviser, invite them to work with you in your Debitoor account. Accountant access in Debitoor lets your accountant, agent, or tax adviser access, view, and export your data, making it easier to get the help you need while eliminating the need for paper and files.