As a freelancer or entrepreneur, you’ll regularly spend money on your business, and if you manage your business’s bookkeeping and accounting, it’s important to know how to account for the purchases you make – which involves distinguishing between assets and expenses.

In this blog post, we explain how an asset differs from an expense, how to account for assets and expenses, and how to record both in your accounting and invoicing software.

Is an asset the same as an expense?

As both assets and expenses are incurred when you buy goods or services for your business, it’s easy to assume that they’re the same thing; however, they're actually quite different.

On the one hand, an asset:

- Is a resource owned by your business

- Helps your business produce goods or provide services

- Usually decreases in value over time.

Assets can be both long-term and short-term, as well as tangible (physical) or intangible (non-physical). Intellectual property, PP&E, and goodwill are all examples of assets.

On the other hand, an expense:

- Is a cost related to the day-to-day running of a business

- Is deducted from revenue in order to calculate profitability.

Examples of expenses include utility bills, rent, payroll, and petty cash.

How to account for assets and expenses

Assets and expenses represent very different things on a business’s financial statements, and the way you should account for an expense is very different to the way you should account for an asset.

Accounting for expenses

Expenses are recorded on the debit side of the profit and loss report, which is also known as an income statement and measures a business’s revenue and losses. According to the principles of double-entry bookkeeping, when you record an expense as a debit, you should also create a credit in another account (usually an asset account or a liability account).

The period in which the expense should be recorded depends on which accounting method you use. If you use accrual accounting, you should record the expense in the period in which the expense is incurred. If you use cash accounting, you should record the expense in the period in which cash changes hands.

For example, you receive an invoice for a utility bill at the end of August, but you don’t actually pay the bill until September. Under the principles of accrual accounting, the expense is recorded in August, which is when the expense was incurred. Under the principles of cash accounting, the expense is recorded in September, which is when cash actually changed hands.

Accounting for assets

Assets are found on the balance sheet along with liabilities and equity or capital. The balance sheet shows how much your business is worth at a specific point in time.

Because assets add value to businesses over an extended period of time, it’s important that this added value is accurately weighed up against the initial cost of the asset. It’s also important to ensure that your accounts reflect the asset’s declining value.

In order to do this, assets are accounted for by following a process called depreciation, which both spreads the cost of the asset throughout its useful life and recognises that the asset loses value over time.

For example, your business makes and sells clothes, and you purchase a sewing machine for £3,000. The sewing machine adds value to your business by enabling you to create the clothes you sell. The sewing machine will last ten years before it needs to be replaced by a newer model. Although the sewing machine is useful and valuable throughout the entire ten years, it's more efficient when it's new and enables you to clothes more quickly in the first few years.

If the sewing machine was recorded as a regular expense, the initial £3,000 cost would only be recorded in the year in which it was bought, and your accounts would not reflect the value the machine adds throughout the remaining nine years. By depreciating the asset throughout its useful life, you allocate the cost of the asset according to the amount of value it adds to your business, which gives a more accurate picture of what your business is actually worth.

How to record assets and expenses with Debitoor invoicing software

It’s easy to record and account for assets and expenses with invoicing software like Debitoor. Expenses can be created in both the Debitoor web app or the Debitoor mobile app, and we have a quick tutorial that gives step-by-step instructions on how to record an expense with Debitoor.

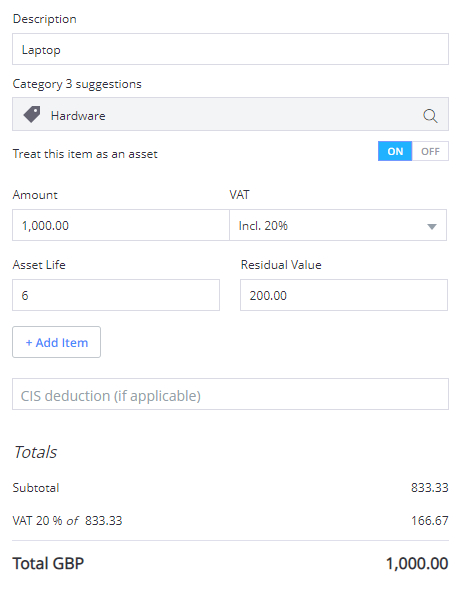

Assets can be recorded from the Debitoor web app. To do this, go to the ‘Expenses’ tab, click on ‘New expense’, and start to fill in the details of the asset (e.g. the price, the supplier, and a brief description).

Based on the description you provide, our system will automatically suggest a few relevant business expense categories. Certain expense categories indicate that the expense is actually an asset, and by selecting one of these categories, you’ll be able to enter a few extra bits of information that enable the expense to be treated as an asset.

Once you enter the asset’s expected useful life and residual value, Debitoor will automatically calculate depreciation expenses using the straight-line method of depreciation. The asset will then appear on your balance sheet, and your depreciation expenses will be shown on your profit and loss statement.