In the UK, businesses with a turnover of £150,000 or less have the option of using cash accounting. Whereas traditional accounting (which is also called accrual accounting) records income and expenses on the date that an invoice is issued, cash accounting recognises transactions on the date that money changes hands.

This blog post explains why it’s important to use invoicing software that allows you to choose your method of accounting, as well as how to activate and use cash accounting in Debitoor.

Cash accounting in your invoicing software

If you use invoicing software to issue invoices, track expenses, and generate financial reports, you need to use software that’s compatible with the way you manage your accounts. This means that if you manage your accounts on a cash basis, your invoicing software must recognise transactions when payments are made (and not when invoices are issued).

Cash accounting and financial reports

While your method of accounting might not have much of an impact on the way you send invoices or manage expenses, cash accounting can have a big effect on the figures in your financial reports.

Your profit and loss reports summarise your costs, expenses, and revenues within a specific period of time (usually a month, quarter, or financial year). The period in which transactions are recorded can vary according to which method of accounting you use, so it’s important that your invoicing software is able to accurately assign costs, expenses, and revenues to the correct period.

For example, you place an order for £200 of office supplies in December 2019; you receive an invoice with payment terms of 30 days, and you pay in January 2020. According to the accrual method of accounting, the expense occurred in December, so the £200 would be considered part of your 2019 turnover. Following the principles of cash accounting, the expense should be recorded in 2020, and the £200 would count towards your 2020 figures

If you manage your accounts on a cash basis but don’t use invoicing software with cash accounting (or forget to activate it in your account settings), you won’t be able to create profit and loss reports that accurately reflect your business’s finances. You might create reports that imply that you’ve spent or received more money than you actually have, and the figures in your profit and loss reports might not match the figures your accountant is working with.

On the other hand, invoicing software with cash accounting allows you to create profit and loss reports that show exactly how much money has changed hands within a specific period of time.

Cash accounting and VAT Returns

UK businesses with a turnover of £1.35 million or less are often able to use the Cash Accounting VAT Scheme, which allows participating businesses to record their VAT according to the principles of cash accounting.

If you use the Cash Accounting VAT Scheme, you’ll therefore record your VAT on the dates that you pay suppliers or receive money from customers, rather than on the dates that you issue or receive invoices.

Since HMRC launched the Making Tax Digital initiative in April 2019, it’s been possible to report your VAT directly from your invoicing software. By activating cash accounting in your invoicing software, you can make sure that you report your VAT on a cash basis.

How to use cash accounting in Debitoor invoicing software

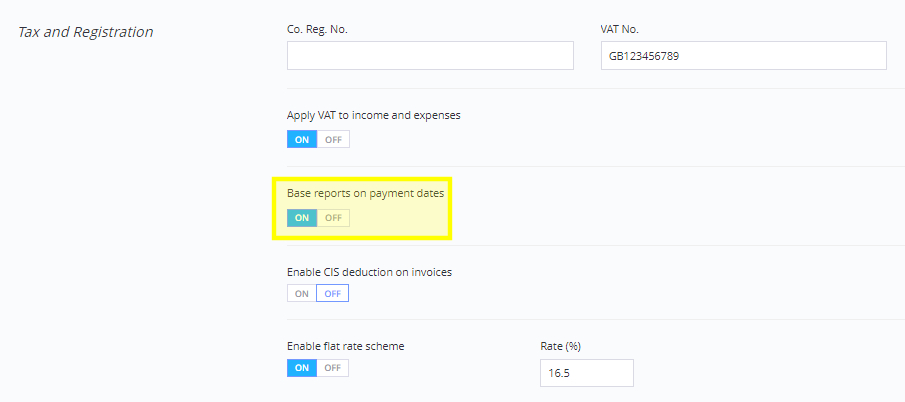

It’s easy to use the cash method of accounting with Debitoor invoicing software. To activate cash accounting in your Debitoor account, go to the ‘Company’ section of your account settings. Under ‘Tax and Registration’, you’ll see an option to ‘Base reports on payment dates’ – click ‘On’.

Once you’ve activated cash accounting in your account settings, your financial reports will be based on the dates that you receive or make payments (rather than the date the invoice or expense was created).

How to enter payments for invoices and expenses

Bear in mind that if you use cash accounting, your income and expenses won’t appear in your financial reports until you create a payment.

To mark an invoice as paid, go to the invoice then click on ‘Enter payment’. You can then create a cash payment or select a bank transaction.

Similarly, if you record expenses in your Debitoor account, you can enter a payment by going to the expense and clicking on ‘Enter payment’.

How to enter payments with automatic bank reconciliation

Alternatively, you could use automatic bank reconciliation, which makes it easier to match invoices and expenses with the incoming and outgoing transactions on your bank statement.

Simply download your bank statement from your online account then upload the .csv file. Debitoor will automatically match the transactions on your bank statement with the invoices and expenses in your account.

Check out our tutorial on using automatic bank reconciliation in Debitoor, or try it for free with our seven-day trial.